A late start to the spring construction season as weather conditions improve and wildfires in critical lumber-producing regions in Canada, including Alberta and Nova Scotia, could impact lumber volumes for flatbed carriers. Focusing on the freight-intensive single-family home building segment, higher interest rates, and construction costs have slowed development significantly. According to the National Association of Home Builders (NAHB), the slowdown is less pronounced in lower-density markets. Meanwhile, multifamily market growth remained strong throughout the nation, according to the latest findings from the National Association of Home Builders (NAHB) Home Building Geography Index (HBGI) for the first quarter of 2023.

According to NAHB Chairman Alicia Huey, “This latest data indicates that the pace of single-family construction in the first quarter of 2023 has slowed from pandemic-induced highs, but a turning point is coming into view with a rebound led particularly in more affordable, lower density areas. And while many builders are having difficulties with labor shortages and tighter financial conditions, the multifamily building market remains strong with risks of slowing later this year.” The HBGI is a quarterly measurement of building conditions across the country. It uses county-level information about single- and multifamily permits to gauge housing construction growth in various urban and rural geographies.

The NAHB reported the lowest single-family year-over-year growth rates in the first quarter of 2023 occurred in large metro core counties, which posted a 25.6% decline. All large and small metro areas also had double-digit negative growth rates. At the same time, rural markets (defined as micro counties and non-metro counties) recorded negative growth rates in the single digits. Over the past four years, rural markets have exhibited particular strength. The rural single-family home building market share has increased from 9.4% at the end of 2019 to 12% by the first quarter of 2023.

Market Watch

All rates cited below exclude fuel surcharges unless otherwise noted.

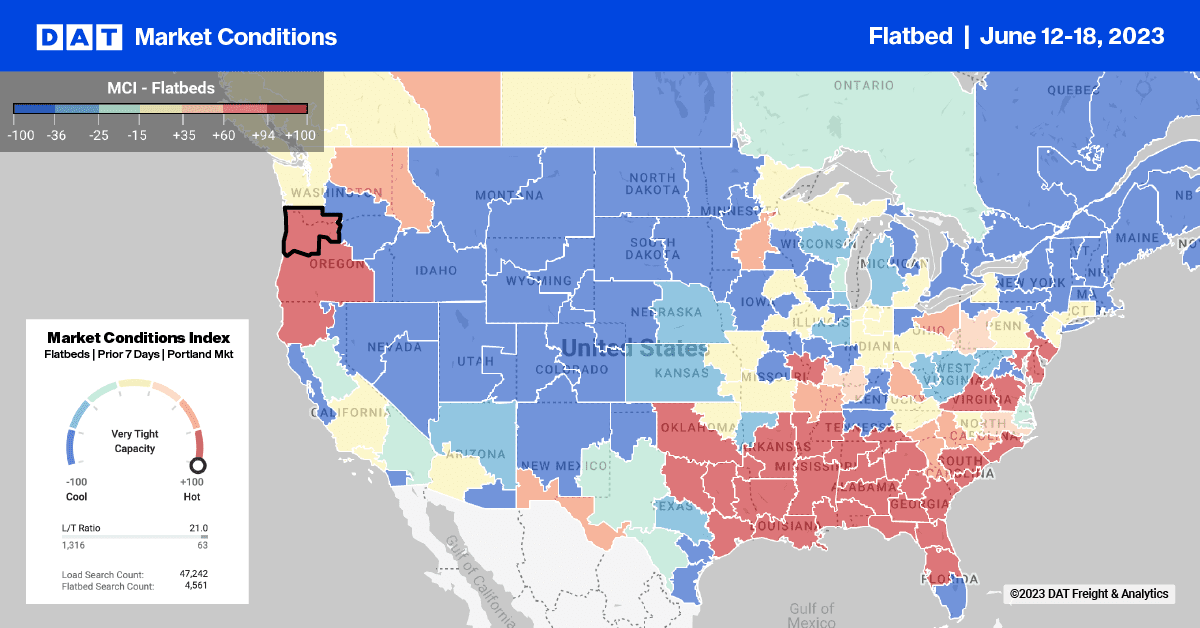

After tracking identically to 2018, Texas outbound average spot rates have lost $0.10/mile since May, impacted by declining oil and gas exploration. The Baker Hughes Rig Count has dropped for the seventh week and is now 7% lower than the previous year’s, impacting flatbed volumes of steel pipe and casing destined for the Permian Basin, where over half of the nation’s drilling rigs reside. At $2.38/mile, loads from Houston to Lubbock are the lowest in 12 months and $1.35/mile lower than in June last year.

Dallas outbound flatbed rates increased by $0.03/mile last week to $2.31/mile, with nearby Ft. Worth rates increasing by the same amount to $2.29/mile. Loads moving on the high-volume lane between Houston and Ft. Worth have decreased by 9% in the last month resulting in spot rates dropping by $0.18/mile over the same timeframe to an average of $2.79/mile.

At $2.58/mile, outbound flatbed rates in Georgia are up $0.09/mile in the last week, led by gains in the Tifton short-haul market, where rates increased $0.06/mile to $2.57/mile. In Jacksonville, linehaul rates increased by $0.08/mile to $2.47/mile, while in the slightly large regional markets in Montgomery and Birmingham, spot rates increased by a penny per mile to $2.81/mile and $2.67/mile, respectively.

Load-to-Truck Ratio (LTR)

Flatbed volumes have dropped almost 20% in the last month following last week’s 13% w/w decrease. Load posts were 34% lower than in 2019 and 72% lower than the previous year. Carrier equipment posts were flat last week, resulting in last week’s flatbed load-to-truck (LTR) ratio decreasing by 13% w/w from 10.66 to 9.31, the lowest since 2016.

Spot Rates

Flatbed linehaul rates have lost almost $0.06/mile in the last fortnight following last week’s $0.02/mile decrease. At a national average of just over $2.13/mile, spot rates are closer to this year’s long-term average following the tightening of flatbed capacity right before Roadcheck Week. Spot rates are $0.42/mile lower than last year and $0.16/mile higher than in 2019.